ACCESS THE METHODOLOGY BELOW

The three phases for building out the turn impact-adjusted curves:

Phase 1: Improved Methodology for deriving the Standard tenors

- Contributed Bank and Broker prices are pre-screened for accuracy.

- Only quality contributors are blended to provide rates for the standard tenors. Inclusion criteria include:

- Active contribution (Min update rate of 1 min/ 5 mins for less liquid pairs e.g. NDFs)

- All contributors for a given currency pair & tenor are blended to create a midcurve

- Bid/ Ask spread is applied looking at the top quartile (25%) of tightest spreads - The end result is much improved standard tenors, which are then used as the basis to imply the turn-impacted forward rates.

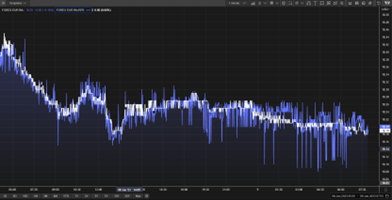

Above 1 min intraday chart compares standard market pricing (blue) & the new “RFB” Turnimpact adjusted FX forwards (White) for the 1 month EURUSD swap-points.

Phase 2: The curves take into account the impact of the turn-dates that take place at (e.g.) Month-end, Quarter-end, Year-end & other key market events such as IMM dates (as described above)... to analytically imply the FX Fwd Points

Methodology (High level summary and assumptions)

- Calculations make use of the continuously compounded forward-forward interest rate differentials implicit in the quoted FX forwards curve.

- Basic assumptions are:

- The interest rate differential is constant in any forward-forward period between quoted tenors that is free of turns

- In a forward-forward period that includes a turn, the interest rate differential is constant for all non-turn days

- When the turn points are not provided as an input, a further assumption is required to calibrate them. In this case we assume that the rate differential for non-turn days in the turn period is the average of rate differentials in the preceding and subsequent periods.

- The turn points are calibrated and/or inserted in the given curve of quoted FX forwards tenors in such a way as to satisfy the above assumptions.

(Note: the calculation for end of month turn-dates does not rely on any market data input for interest rates, but only on implicit rate differentials from FX forwards quotes. One would obtain similar results by using one-day averages of forward-forward points as the basis of calculation.)

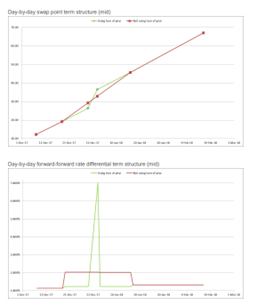

The examples below show how the turn calibration method reflects the discontinuous nature of the turn impact, while keeping a “natural” progression of the term structure over non-turn days

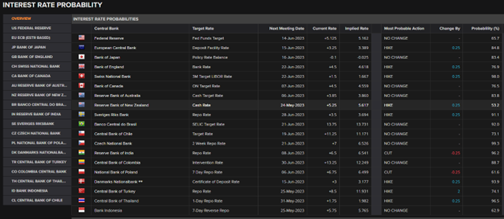

Central Bank turn-impact adjustments account for changes in the interest rate differential following anticipated rate decisions.

- Probability based models provide the expected outcome for future Central Bank meeting rate decisions. LSEG FX uses a proprietary model to determine the likely outcome for future rate decisions.

- The impact from probability weighted future Central Bank rate expectations, together with the OIS curve are used to model a “Constant Forward Rate” which best describes the interest rate differential following the rate decision.

- The Central Bank turn-adjusted FX Forward is implied using the “expectation based” relative constant forward rates following the rate decision.

Phase 3: FXall historical trades (post trade data) for the turn dates are used to calibrate the analytically derived FX swap points.

LSEG FX Venues enable FX trades averaging over US$460 billion daily across Spot, FX Forwards, NDFs & FX Options. This provides a considerable pool of post trade observations which we use to calibrate our curve methodology and assumptions.

LSEG FX “turn-date Impact-adjusted” FX Forward Curves.

LSEG FX has deployed this best practise methodology, leveraging the breadth of data, analytics and liquidity available within LSEG FX to provide a full suite of turn-date impact-adjusted forward FX curves across a broad range of currency pairs (available on Workspace via page FXBD, via quote <FXBLEND>, or FX Forwards analytics FWDS)

FX Forward points including the following turn-date tenors:

- Beginning and End of month FX Fwd points

- Beginning and End of quarter FX Fwd points

- Beginning and End of year FX Fwd points

- IMM Dates (March, June, September & December)

- Central Bank rate decision tenors will be added in Q3 ’23

The FX Forward Curves are also available via API over our Elektron/ RDP data feed to help FX market participants automate & improve their trading workflow including:

- Price Discovery for trading

- Client pricing

- Mid and Back-office processes including: Risk Management, Valuation/ MtM, TCA reference rate, Surveillance etc.)

For more information, please contact your LSEG Account Manager.